Bidding wars are frustrating. You find the perfect home, schedule an appointment immediately, and within a day there are already multiple offers on it. Common knowledge is that bidding wars mean you have to pay more than the asking price, and often get creative with removing some terms. If you’re somebody who has been looking for a long time because you don’t want to overpay for a home, read this. It might help you gain some perspective that helps your unique situation:

This idea came from a conversation I had with a buyer this weekend. I took somebody to look at a home that we just put up on the market whom I had never met before. I started chatting with her, and it came up how long she had been looking for a home. She said that she had been looking for a year. Naturally, I wanted to know why she had been looking for so long. She said it was the price and that, looking at the top of her budget, she didn’t want to overpay for a home or get into a bidding war.

This blog today is specifically for people who are in that boat. Maybe I can give you a different perspective moving forward. So many people get hung up on just the purchase price, and they don’t look at the big picture when it comes to buying a home and all of the financial costs that go with it.

I want to put out a simple disclaimer. This advice is not for people who genuinely feel they can’t afford to buy a home or are looking at the top of their budget, and they can’t afford to get into a bidding war. This advice is for people looking for a home, and they are not pulling the trigger simply because they do not want to pay over market value

1. Increasing Home Values

So, I am going to use an example here. Let’s say $200,000 is your budget, which is a very fair first-time home buyer budget. If you were looking at the beginning of 2020, and now you’re looking again, homes in the $200,000 range in my Michigan market (Plymouth, Northville, Novi, Canton, and the surrounding communities) have gone up 12%. So, that $200,000 home you were looking at a year ago is worth about $224,000 now. That is a $24,000 bump! Now, you either have to buy less of a home for your $200,000 budget, or hopefully, your budget has gone up, so now you can afford to pay that additional $24,000.

2. When You Overpay, You Are The New Comp

When you get into a bidding war, you have to overpay for your home. Sometimes this leads to starting off with negative equity. In a seller’s market, this is happening everywhere. Remember, when you pay over market value, and then another buyer does, and then another, you all just became the new comps. You all set the new price standard. That is how home values go up in general. So even though at that moment you had to overpay for that home, if the market is a hot seller’s market, then the other houses around you are doing the same thing. You become the baseline, and then you don’t have negative equity anymore.

This is how home values went up 12% in my last example. The owners who overpaid for that $200,000 home at the beginning of 2020 just made their equity back. Everyone buying in 2021 has to pay even more than they did to get into the neighborhood.

3. Rising Interest Rates

If you are getting a mortgage, you have an interest rate you have to pay. Right now, interest rates are at all-time lows. There’s a good chance they’re going to go back up into the 3%-4% range soon. I am going to use 3.5% for my example.

Sticking with that $200,000 budget, if your rate went from 3.5% to 4.5% while you were waiting to time the market, you now have an additional $100 per month you would pay in just interest. Over the course of 30 years, that adds up to about $33,000. This is one of those hidden costs people often overlook when buying a home. Again, just a way to think about the big picture.

4. Paying More in Taxes

The property taxes you pay on a home are based off an assessed value, or State Equalized Value (SEV). This number is determined by the county, and how much they go up or down every year is determined by them and the market.

When you buy a home, your taxes will be based off of that SEV. Once you own the home, Michigan has laws to protect you from having huge fluctuations in the amount of property tax you pay. It says that your property taxes can only increase by the rate of inflation, but not more than 5%. This means that if inflation was 10%, your taxes only go up by 5%.

This is the reason taxes usually “go up” when you buy a home. You’re able to see the amount the current owner is paying, but that number often reflects years of them living there.

In an appreciating market, it makes sense to buy a home sooner so that you can lock in that 5% max tax increase. Otherwise, you end up paying taxes based off of market value, or SEV, which is often higher.

5. Timing The Market Doesn’t Matter If You’re Buying Long Term

What if this is the peak though? What if the market is bound to take a dip soon? My examples that I’ve been using are based off of the assumption that prices are increasing. For the record, all of the marjor real estate data companies show prices increasing again throughout 2021. The real estate market has shown that it’s resilient, because it thrived during a pandemic shutdown.

With that said, there’s always a chance the market shifts to a buyers market. It’s normal for the market to breathe a bit before it goes up again, and we’ve been going up for a long time.

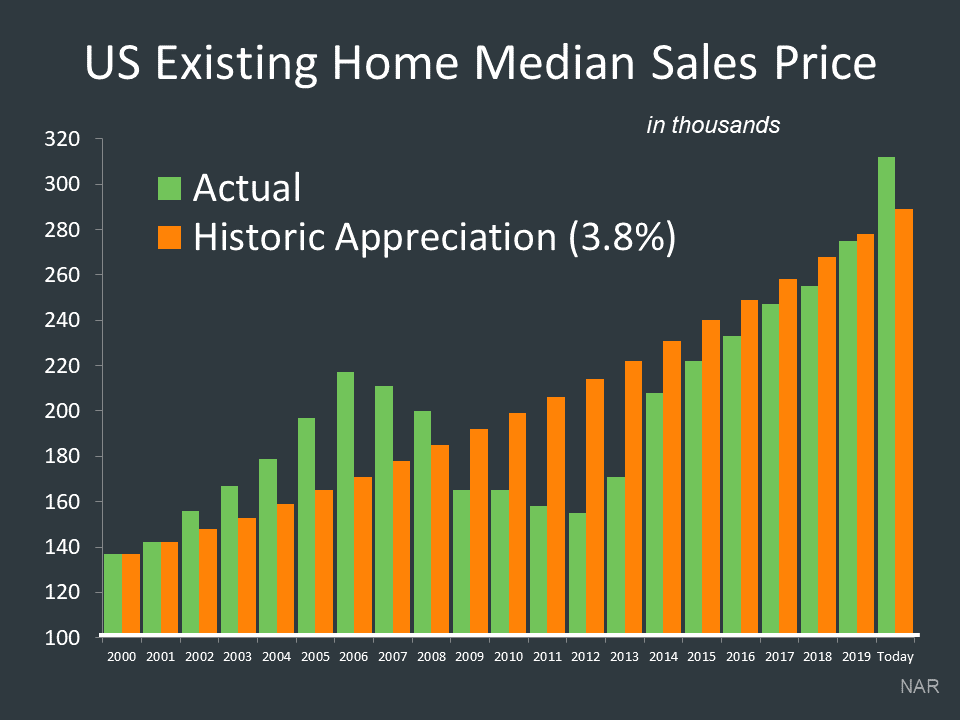

The good news? If you’re buying in the long term, none of that matters. U.S. housing prices have historically appreciated at 3.8% over time. Even the people who bought at the last peak during the housing bubble of the mid-2000’s have earned their value back. Here is a graph showing what home prices have done over the last 20 years compared to the historic 3.8% appreciation:

You can see that despite the major swings in home prices over the last 20 years, we’re still right in line with the historic average. So, if you’re buying a home to live in then you can rest a little knowing that even if prices go down, history tells us they’ll go up again.

If you’re buying in the short term, I still stand by everything previously discussed in this article. I recommend that you simply not max out your budget, because it’s a temporary home. If the alternative is renting, find something that is comfortable with your budget, even if you have to overpay for the property. This way you aren’t as impacted by any market swings, and you’re able to put aside the extra cash you would have been paying toward your mortgage had you maxed out your budget.

In Conclusion

Hopefully this brought you value and helps you make an educated decision. Buying a home has a lot of financial and opportunity cost involved. Purchase price is just one part of the equation, and I’ve seen too many buyers get “priced out” of the market because prices went up while they waited to buy.

I understand not wanting to overpay for anything. I’m a coupon clipper myself, and am always looking to find a good deal. In a complicated financial purchase/investment like buying a home, sometimes it pays to overpay. Or maybe better, it costs less to overpay.

Have a great day! Stay safe.